If you don't file your tax return, the IRS charges a failure-to-file penalty of 5% of the unpaid tax per month (capped at 25% after five months), while filing on time but not paying costs only the 0.5% per month failure-to-pay penalty, also capped at 25%. Filing, even when you can't pay a dollar of the bill, cuts your monthly penalty rate by 90%. And a never-filed year has no statute of limitations: the IRS can assess that tax 5, 10, or 20 years later.

Key takeaways:

- Failure-to-file penalty: 5% per month, max 25% (IRC §6651(a)(1)); failure-to-pay penalty: 0.5% per month, max 25% (IRC §6651(a)(2))

- Returns filed 60+ days late owe a minimum penalty of $525 or 100% of the tax due, whichever is less (returns due in 2026)

- Interest runs at 7% (Q3 2026), compounded daily, on both tax and penalties, and cannot be waived

- If you never file, the IRS can create a Substitute for Return with none of your deductions

- Refunds expire: file within 3 years of the due date or the money is forfeited

The failure-to-file penalty punishes a missing return; the failure-to-pay penalty punishes an unpaid balance. They are separate penalties under IRC §6651, they can run at the same time, and the filing penalty is ten times larger. Here is every consequence of not filing, in one table:

| Consequence | Details |

|---|

| Failure-to-file penalty | 5% of unpaid tax per month, max 25% |

| Failure-to-pay penalty | 0.5% of unpaid tax per month, max 25% |

| Minimum late-filing penalty | $525 or 100% of tax due (whichever is less) for returns 60+ days late |

| Interest | Federal short-term rate + 3% (7% in Q3 2026), compounding daily |

| Substitute for Return (SFR) | IRS files a return for you, without your deductions |

| Tax lien | Public claim against your property |

| Tax levy | Seizure of wages, bank accounts, or property |

| Criminal prosecution | Up to 1 year jail + $25,000 fine (misdemeanor under IRC §7203) |

| Statute of limitations | None: the IRS has unlimited time if you don't file |

Legal basis: IRC §6651 (penalties), IRC §6654 (estimated tax penalty), IRC §7203 (criminal failure to file), IRS Publication 17

The failure-to-file penalty is the IRS's primary tool for encouraging timely filing. It is significantly steeper than the failure-to-pay penalty, by design.

- Rate: 5% of the unpaid tax for each month (or partial month) your return is late

- Maximum: 25% of the unpaid tax

- Timeline: The penalty starts on the day after the filing deadline (April 15 for most individual returns) and accrues each month

Worked example: you owe $10,000 in tax and don't file.

| Months late | Penalty added | Cumulative penalty |

|---|

| Month 1 | $10,000 × 5% = $500 | $500 |

| Month 2 | $500 | $1,000 |

| Month 3 | $500 | $1,500 |

| Month 4 | $500 | $2,000 |

| Month 5 | $500 | $2,500 (25% cap reached) |

The penalty reaches its 25% maximum after just 5 months. That means your $10,000 tax bill becomes $12,500 before interest is even calculated.

If your return is more than 60 days late, the minimum failure-to-file penalty is the lesser of $525 or 100% of the tax due. This minimum applies for returns required to be filed in 2026.

This means even if you only owe $200, the minimum penalty is $200 (100% of tax due). If you owe $1,000, the minimum penalty is $525.

If your return would result in a refund or zero balance, there's technically no penalty for filing late because the penalty is calculated as a percentage of unpaid tax (which would be $0). However, you must file within 3 years of the original due date to claim your refund — after that, you forfeit it permanently.

Separate from the filing penalty, the IRS charges a penalty for not paying your tax by the due date.

- Rate: 0.5% of the unpaid tax for each month (or partial month) the tax remains unpaid

- Maximum: 25% of the unpaid tax

- Reduced rate: If you file on time and set up an installment agreement, the rate drops to 0.25% per month

- Increased rate: If the IRS issues a Notice of Intent to Levy and you don't pay within 10 days, the rate increases to 1% per month

When both penalties apply at the same time (you didn't file AND you didn't pay), the failure-to-file penalty is reduced by the failure-to-pay penalty for the same month. This means:

- Months 1–5: Combined penalty is 5% per month (4.5% filing + 0.5% payment)

- After month 5: Only the failure-to-pay penalty continues at 0.5% per month (the filing penalty has maxed out)

- Maximum combined: 47.5% of unpaid tax (25% filing + 22.5% payment over 50 months)

| File Late, Pay Late | File on Time, Pay Late |

|---|

| Month 1 | 5% total | 0.5% total |

| Month 5 | 25% total | 2.5% total |

| Month 12 | 28.5% total | 6% total |

The takeaway: Filing on time, even without payment, reduces your total penalties by roughly 80% over the first year.

On top of penalties, the IRS charges interest on any unpaid balance. Interest applies to both the unpaid tax and any accrued penalties.

- Rate: Federal short-term rate + 3 percentage points. For the third quarter of 2026 the underpayment rate is 7% (Rev. Rul. 2026-10); the rate resets quarterly and was 7% in Q1 2026 and 6% in Q2 2026

- Compounding: Interest compounds daily, not monthly

- Start date: Interest begins on the original due date of the return, regardless of extensions

- No maximum: Unlike penalties, there's no cap on interest. It accrues until you pay in full

Worked example: $10,000 of unpaid tax at a steady 7% annual rate, compounded daily, with no payments made:

| Time elapsed | Balance (interest only) |

|---|

| After 1 year | ~$10,725 |

| After 2 years | ~$11,503 |

| After 3 years | ~$12,337 |

| After 5 years | ~$14,191 |

This is interest alone, before any penalties, and the actual figure shifts as the quarterly rate changes.

Important: Interest cannot be waived or abated, even if you qualify for penalty relief. The IRS has the authority to remove penalties in certain circumstances, but interest charges remain.

If you don't file but the IRS has information about your income (from W-2s, 1099s, bank reports, or other third parties), they can file a return on your behalf. This is called a Substitute for Return (SFR) under IRC §6020(b).

The IRS prepares an SFR using only the income information they have. They do NOT include:

- Business deductions (Schedule C expenses)

- Itemized deductions

- Tax credits you qualify for (child tax credit, education credits)

- A favorable filing status (SFRs use single or married filing separately, even if head of household would save you more)

- Self-employment tax deduction (the 50% deduction)

For self-employed filers, this is devastating. If clients sent 1099-NEC forms showing $80,000 in income, the IRS puts $80,000 on your SFR without any of the $30,000 in legitimate business expenses you could have claimed. Your tax bill on the SFR will be dramatically higher than what you'd actually owe if you filed your own return.

- The IRS sends you a Notice of Deficiency (CP3219A) showing the proposed tax

- You have 90 days to file a petition with the Tax Court if you disagree

- If you don't respond, the assessment becomes final

- The IRS begins collection actions on the assessed amount

- Penalties and interest accrue from the original due date

Even after the IRS files an SFR, you can file your own return with your actual income, deductions, and credits. In most cases, filing your own return will significantly reduce the amount owed. There is no time limit on filing your own return to replace an SFR, but the sooner you do it, the less interest and penalties accumulate.

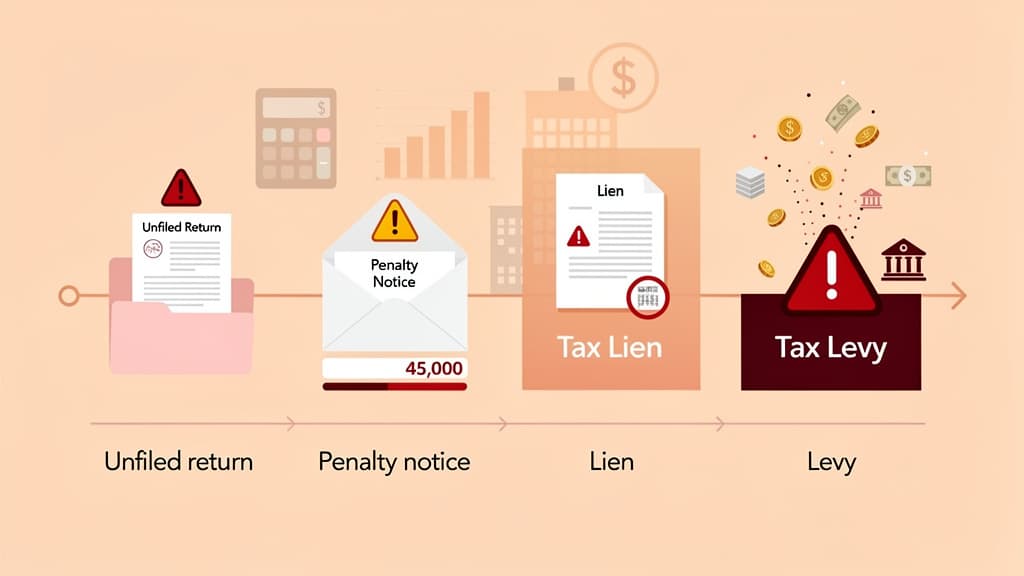

If you don't file, don't pay, and don't respond to IRS notices, enforcement actions escalate:

A federal tax lien is a legal claim against all your property: real estate, vehicles, bank accounts, securities, business assets. It's not a seizure; it's a claim that takes priority over other creditors.

- The lien attaches to all current and future property

- It appears on your credit report and can severely damage your credit score

- It makes it difficult to sell property, refinance a mortgage, or get a loan

- The lien remains until the tax debt is paid in full or the collection statute expires (generally 10 years from assessment)

Under the IRS Fresh Start Initiative, the IRS will generally withdraw a tax lien once you enter into a Direct Debit installment agreement and owe $25,000 or less.

A tax levy is an actual seizure of your property or income. Unlike a lien, a levy takes your money or assets.

The IRS can levy:

- Wages: your employer must turn over a portion of each paycheck

- Bank accounts: the IRS freezes your account and seizes the balance after 21 days

- Social Security benefits: up to 15%

- Accounts receivable: money owed to your business by clients

- Real property: your home (requires approval from an IRS district director)

- Vehicles and other personal property

Before levying, the IRS must:

- Assess the tax and send a Notice and Demand for Payment

- Wait for you to neglect or refuse to pay

- Send a Final Notice of Intent to Levy at least 30 days before the levy

If you owe $66,000 or more in seriously delinquent tax debt (the 2026 threshold, adjusted annually for inflation, including penalties and interest), the IRS can certify your debt to the State Department, which may deny or revoke your passport.

In the most extreme cases, willful failure to file a tax return is a federal crime.

Under IRC §7203, any person required to file a tax return who willfully fails to do so is guilty of a misdemeanor. Upon conviction:

- Fine: Up to $25,000 ($100,000 for corporations)

- Imprisonment: Up to 1 year

- Plus: Costs of prosecution

Criminal prosecution requires proof that you knew you had a legal obligation to file and deliberately chose not to. Simply forgetting, being disorganized, or not being able to afford professional preparation is not willful failure.

The IRS typically pursues criminal charges when:

- The taxpayer has high income and clearly knew about the filing requirement

- There's a pattern of deliberate non-filing over multiple years

- The amounts involved are significant

- The taxpayer actively concealed income or assets

Criminal prosecution for failure to file is relatively uncommon. The IRS Criminal Investigation division pursues around 2,000–3,000 investigations per year across all tax crimes, and only a fraction involve pure failure-to-file cases. However, the consequences are severe enough that the risk shouldn't be ignored.

The statute of limitations for criminal prosecution under §7203 is 6 years from the date the return was due.

If you haven't filed for several years, each year is a separate violation accruing its own penalties, and none of those years ever closes. The audit clock only starts when a return is filed:

| Scenario | Statute of Limitations |

|---|

| Filed a return | IRS has 3 years to audit (6 years if 25%+ understatement) |

| Never filed a return | No limit — the IRS can assess tax at any time |

| Filed a fraudulent return | No limit |

This is the most compelling reason to file. Once you file a return, the 3-year clock starts running. If you never file, the IRS has unlimited time to come after you. Multiple unfiled years also stack: three unfiled returns with $10,000 due each can mean $7,500 in filing penalties alone, plus failure-to-pay penalties and daily interest on all three balances. In practice, the IRS generally asks non-filers for the last 6 years of returns to get back into compliance (covered below). We explain how filed returns get selected for exams in our IRS audit triggers guide.

The IRS doesn't rely on voluntary disclosure. They have multiple systems to identify people who should be filing but aren't:

The IRS receives copies of all W-2s, 1099-NECs, 1099-MISCs, 1099-Ks, and other information returns. Their Automated Underreporter (AUR) system matches these documents against filed returns. No return + income documents = automatic flag.

Banks report interest income. Brokerages report investment income. Payment processors report transactions. Even cryptocurrency exchanges now report sales. If money is flowing to you, the IRS likely knows about it.

The IRS shares data with state tax agencies. If you file a state return but not a federal return (or vice versa), the discrepancy will be flagged.

If you're self-employed and don't file, the SSA won't credit your self-employment income toward your Social Security benefits. You'll miss out on retirement and disability credits, and the gap creates a mismatch that the IRS can detect.

If you haven't filed one or more tax returns, here's the step-by-step process to get current. At Anna Money, where we served 60,000+ SMEs, we watched owners let one missed filing snowball for years because re-engaging felt scarier than hiding; the fix is the same in the US: file first, negotiate payment second.

Collect all income documents (W-2s, 1099s) and expense records for each unfiled year. If you've lost documents, you can request a Wage and Income Transcript from the IRS (Form 4506-T) to see what income they have on file for each year.

File your past-due returns as soon as possible. There's no limit on how far back you can file, but the IRS typically requires the last 6 years of returns to consider you in compliance.

Important for self-employed filers: Filing your own return, even years late, is almost always better than letting the IRS file an SFR. Your return will include business deductions and credits the SFR ignores, significantly reducing your tax bill.

If you can pay the full balance, do so. If you can't, file anyway and explore payment options:

IRS Installment Agreement

- Short-term (180 days or less): no setup fee; apply online if you owe under $100,000 in combined tax, penalties, and interest

- Long-term (monthly payments): apply online if you owe $50,000 or less (including penalties and interest)

- Setup fee: $22 (online, direct debit) up to $178 (applying by phone, mail, or in person without direct debit); reduced or waived for low-income taxpayers

- Failure-to-pay penalty drops to 0.25% per month while the agreement is active

Offer in Compromise (OIC)

- The IRS agrees to settle your tax debt for less than the full amount owed

- You must demonstrate inability to pay the full amount within the collection statute

- Application fee: $205 (waived for low-income taxpayers)

- Acceptance rate: approximately 30-40% of applications

Currently Not Collectible (CNC) Status

- If paying anything would prevent you from meeting basic living expenses, the IRS can temporarily suspend collection

- You must provide a detailed financial statement (Form 433-A or 433-F)

- Penalties and interest continue to accrue, but no active collection occurs

- The IRS reviews your financial situation periodically

The IRS may waive penalties (though not interest) if you can show reasonable cause for your failure to file or pay. Common reasonable cause arguments include:

- Serious illness or hospitalization

- Death of an immediate family member

- Natural disaster

- Fire, casualty, or other loss of records

- Reliance on incorrect advice from a tax professional

- IRS errors or delays

For first-time offenders, the IRS offers First Time Penalty Abatement (FTA): an administrative waiver for taxpayers with a clean compliance history for the prior 3 years.

If you're self-employed and didn't file, you also likely missed quarterly estimated tax payments. The estimated tax penalty (IRC §6654) applies separately from the failure-to-file and failure-to-pay penalties.

Use our 1099 tax calculator to estimate what you owe and plan your payments.

Even if you can't pay income tax, self-employment tax (15.3% on net earnings: 12.4% Social Security + 2.9% Medicare) is a separate obligation. The IRS collects SE tax through your filed return.

If you're self-employed and don't file a return, your self-employment income won't be reported to the Social Security Administration. This means you won't earn credits toward Social Security retirement or disability benefits, credits you cannot recover later.

Self-employed filers have additional deadlines beyond April 15. See our guide on when business taxes are due for a complete calendar.

Mistake #1: Assuming the IRS won't notice. They will. Information matching systems are automated. Every W-2 and 1099 sent to you is also sent to the IRS. It may take a year or two, but non-filer cases are identified systematically.

Mistake #2: Not filing because you can't pay. This is the most expensive mistake you can make. The failure-to-file penalty (5%/month) is ten times the failure-to-pay penalty (0.5%/month). Always file, even if you can't pay. The IRS has payment plans.

Mistake #3: Waiting for the IRS to contact you first. Coming forward voluntarily before the IRS contacts you gives you more options and better outcomes. You may qualify for penalty abatement. You can claim all your deductions. You control the timeline.

Mistake #4: Believing there's a deadline to file past-due returns. There is no deadline. You can file returns from any prior year at any time. The sooner you file, the sooner the statute of limitations starts running and the sooner you can stop the bleeding of penalties and interest.

Mistake #5: Using a tax preparer who promises to make everything "go away." Be wary of anyone who guarantees a specific outcome with the IRS. Legitimate tax professionals will explain your options honestly — including the possibility that you'll owe taxes, penalties, and interest even with the best strategy.

Unfiled returns usually start with messy records: when a full year of uncategorized transactions is waiting, avoidance wins. Jupid keeps the books ready before the deadline arrives. It connects to your bank accounts and categorizes business transactions automatically with 95.9% accuracy, so income and expenses are already sorted into the right Schedule C categories when it's time to file. The AI accountant answers deadline and deduction questions in WhatsApp or iMessage in real time, and tracks your quarterly estimated payments so this year's return never becomes next year's problem. Try Jupid.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently. Consult a qualified tax professional for advice specific to your situation. Jupid provides automated bookkeeping and tax categorization — we are not a CPA firm or tax advisory service.