There is no deadline to file a past-due federal tax return, but you generally only need to file the last six years to get back into good standing with the IRS (Policy Statement 5-133). File even if you can't pay: the failure-to-file penalty is 5% of the unpaid tax per month, ten times the 0.5% failure-to-pay penalty, and interest runs at 7% for the third quarter of 2026. This guide is the exact sequence to file overdue returns, cap the penalties, and set up a payment plan, whether you are behind one year or ten.

Key takeaways:

- No time limit to file a late return, but the IRS generally asks for the past 6 years to treat you as compliant (Policy Statement 5-133)

- Failure-to-file penalty: 5% per month, max 25%. Failure-to-pay penalty: 0.5% per month, max 25%. Filing stops the bigger one even if you pay nothing

- Interest: federal short-term rate + 3% = 7% for Q3 2026, compounded daily from the original due date, and the IRS generally cannot waive it

- You have only 3 years from the original due date to claim a refund (IRC §6511); miss it and the refund is gone

- Streamlined IRS payment plan covers balances $50,000 or less (up to 72 months); First-Time Penalty Abatement can erase penalties for one clean year

You can file a return for any year, no matter how long ago. To be treated as in "filing compliance" for a payment plan, a loan, or to stop enforcement, the IRS generally wants the most recent six years on file (IRS Policy Statement 5-133).

| Rule | Detail |

|---|

| Time limit to file | None. You can file any year |

| Years to file for compliance | Generally the last 6 years (IRS Policy Statement 5-133) |

| Time limit to claim a refund | 3 years from the original due date (IRC §6511) |

| Failure-to-file penalty | 5% of unpaid tax per month, up to 25% |

| Failure-to-pay penalty | 0.5% of unpaid tax per month, up to 25% |

| Minimum late filing penalty | $525 or 100% of tax due (whichever is less) for returns over 60 days late (returns filed in 2026) |

| Interest on unpaid tax | Federal short-term rate + 3% = 7% for Q3 2026, compounded daily |

| Installment agreement threshold | $50,000 or less for streamlined approval |

| Offer in Compromise | Settle for less than owed if you qualify |

Legal basis: IRC §6511 (refund limitations), IRC §6651 (penalties), IRC §6601 (interest), IRS Policy Statement 5-133 (six-year filing norm), Form 9465 (installment agreement), Form 656 (Offer in Compromise)

Self-employed individuals are more likely to have unfiled tax returns than W-2 employees, and the reasons are structural:

W-2 employees have federal and state taxes withheld from every paycheck. By tax time, most of them are close to breaking even or due a refund. Self-employed individuals have nothing withheld. Their entire tax bill, income tax plus 15.3% self-employment tax, comes due at once.

The IRS expects self-employed individuals to make quarterly estimated tax payments. But when you're busy running a business, those quarterly deadlines (April 15, June 15, September 15, January 15) slip by. Miss a couple of quarters, and the year-end bill becomes intimidating.

Freelancers don't always know what they'll earn in a given year. A great Q4 can push you into a higher tax bracket and create a large unexpected bill. A slow Q1 might tempt you to skip estimated payments that turn out to be needed.

The most dangerous pattern: you owe taxes for Year 1, don't file, and then feel too anxious to file Year 2 because Year 1 is still outstanding. Each year adds to the pile. Penalties and interest accumulate. The problem that started as a $3,000 tax bill becomes a $15,000 problem over three or four years.

The good news: The IRS would rather work with you than against you. Filing, even years late, puts you on a path to resolution.

How many years do you have to file? For most people, the answer is the last six. IRS Policy Statement 5-133 directs the agency to generally enforce delinquent-return filing for no more than the past six years, and the IRS treats a taxpayer who has filed the most recent six years as being in filing compliance for a payment plan, an Offer in Compromise, or to release enforced collection. A revenue officer can require more years when the facts justify it (large potential liability, business returns, an open investigation), but six is the working norm.

Check your records or call the IRS (1-800-829-1040) to find out which years have unfiled returns. You can also:

- Request your IRS account transcript at irs.gov/individuals/get-transcript, which shows which years have returns on file

- Request a wage and income transcript: this shows what income the IRS has recorded for you (1099s, W-2s, etc.)

If the IRS has filed a Substitute for Return (SFR) on your behalf, your transcript will show it. SFRs are filed when the IRS has income information (from 1099s and W-2s sent by your clients and employers) but no return from you. SFRs are almost always worse for you than filing yourself because the IRS claims no deductions or credits on your behalf.

For each unfiled year, collect:

- Income records: 1099-NEC forms, 1099-MISC, 1099-K, W-2s, bank statements showing business deposits

- Expense records: Bank and credit card statements, receipts, mileage logs, home office measurements

- Prior year returns: If you filed some years but not others, prior returns help with consistency and carryforward items

Missing documents? Request wage and income transcripts from the IRS for each year. These show all reported income. For expenses, use bank and credit card statements as backup documentation.

This is critical: you must use the tax forms and rules for the year you're filing. A 2022 tax return uses 2022 forms, 2022 tax rates, and 2022 standard deduction amounts.

Download prior-year forms at irs.gov/prior-year-forms.

Key numbers change annually:

| Tax Year | Standard Deduction (Single) | SE Tax Rate | Social Security Wage Base |

|---|

| 2021 | $12,550 | 15.3% | $142,800 |

| 2022 | $12,950 | 15.3% | $147,000 |

| 2023 | $13,850 | 15.3% | $160,200 |

| 2024 | $14,600 | 15.3% | $168,600 |

| 2025 | $15,750 | 15.3% | $176,100 |

| 2026 | $16,100 | 15.3% | $184,500 |

The 2025 single standard deduction is $15,750 after the One Big Beautiful Bill Act raised it; the 2026 amount is $16,100 (IRS Rev. Proc. 2025-32). The Social Security wage base, the cap on the 12.4% Social Security portion of self-employment tax, rose to $184,500 for 2026 from $176,100 in 2025.

For each year, complete:

- Form 1040: Individual income tax return

- Schedule C: Profit or loss from business (for self-employment income)

- Schedule SE: Self-employment tax

- Schedule 1: Additional income and adjustments (deductible half of SE tax)

- Any other applicable schedules (Schedule A if itemizing, Schedule D for capital gains, etc.)

Claim every deduction you're entitled to. Business expenses, home office deduction, vehicle expenses, health insurance premiums, and retirement contributions all reduce your tax liability. Use our Self-Employment Tax Calculator to estimate what you owe for each year, and the 1099 Tax Calculator to understand your total liability.

E-filing: You can e-file current and prior year returns (typically the current year plus two prior years) using tax software. For older returns, you'll need to file by mail.

Filing by mail: Print and sign each return, then mail it to the appropriate IRS address for your state (the address varies by year and state; check the instructions for each year's Form 1040).

File the most recent years first if you're filing multiple years. The IRS prioritizes recent compliance, and having the most recent years on file shows good faith.

This is the single most important piece of advice in this guide: file even if you can't pay the full amount. The failure-to-file penalty (5% per month) is ten times worse than the failure-to-pay penalty (0.5% per month). Filing the return stops the more expensive penalty from accruing.

- Rate: 5% of unpaid tax for each month (or partial month) the return is late

- Maximum: 25% of unpaid tax

- Minimum: If your return is more than 60 days late, the minimum penalty is the lesser of $525 or 100% of the tax due (for returns required to be filed in 2026)

- Combined with failure-to-pay: If both penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay penalty. The combined maximum is still 5% per month (4.5% file + 0.5% pay).

- Rate: 0.5% of unpaid tax for each month (or partial month) it remains unpaid

- Maximum: 25% of unpaid tax

- Reduced rate: If you set up an installment agreement, the rate drops to 0.25% per month

- Rate: Federal short-term rate + 3%, compounded daily

- Current rate: 7% for the third quarter of 2026 (a 4% federal short-term rate plus 3 points). The IRS resets this rate every quarter, and it has ranged 6%–8% in recent years.

- Key fact: Interest accrues from the original due date of the return, not from the date you file. This means interest is accumulating right now on any unfiled returns where tax is owed.

- No waiver: Unlike penalties, the IRS generally cannot waive interest. It accrues by law.

Here's what happens to a $5,000 tax debt if you don't file or pay:

| Time Period | Failure-to-File | Failure-to-Pay | Interest (~7%) | Total Owed |

|---|

| 1 month late | $250 | $25 | $33 | $5,308 |

| 5 months late | $1,250 (max) | $125 | $167 | $6,542 |

| 1 year late | $1,250 (max) | $300 | $400 | $6,950 |

| 3 years late | $1,250 (max) | $900 | $1,200 | $8,350 |

| 5 years late | $1,250 (max) | $1,250 (max) | $2,000 | $9,500 |

Note: These are simplified estimates. Actual amounts vary based on the quarterly federal short-term rate and compounding.

The longer you wait, the more it costs, but most of the penalty damage happens in the first five months, when the failure-to-file penalty maxes out. After that, it's mostly interest accumulation.

If you can pay your full balance within 120 days, the IRS offers a short-term payment plan with no setup fee. Interest and the failure-to-pay penalty continue to accrue during the 120 days.

Apply online at irs.gov/payments/online-payment-agreement-application.

For balances you can't pay within 120 days:

Streamlined Installment Agreement (if you owe $50,000 or less):

- No detailed financial disclosure required

- Up to 72 months to pay

- Apply online, by phone, or by mailing Form 9465

- Setup fee: $22 (online, direct debit) to $178 (by mail/phone)

- Low-income fee waiver available

Non-Streamlined Installment Agreement (if you owe more than $50,000):

- Requires Form 433-A (Collection Information Statement)

- Financial disclosure of assets, income, and expenses

- IRS determines an affordable monthly payment

An OIC lets you settle your tax debt for less than the full amount owed. The IRS considers:

- Your ability to pay (income and assets)

- Your expenses (allowed living expenses)

- Your future earning potential

Qualifying is difficult. The IRS approves roughly 30-40% of OIC applications. You must be current on all filing requirements and estimated tax payments. There's a $205 application fee (waived for low-income taxpayers) plus an initial payment.

The IRS Fresh Start Initiative expanded OIC eligibility by allowing the IRS to consider only one year of future income (for lump-sum offers) or two years (for periodic payment offers), instead of four or five years under prior guidelines.

If you genuinely cannot pay anything, because your income only covers basic living expenses, you can request CNC status. The IRS temporarily stops collection activity, but:

- Interest and penalties continue to accrue

- The IRS reviews your financial situation periodically

- Tax liens may still be filed

If you have a clean compliance history (filed and paid on time for the past three years), you may qualify for First-Time Penalty Abatement. This removes the failure-to-file and failure-to-pay penalties for one tax period.

You can also request penalty relief for "reasonable cause": serious illness, natural disaster, death in the family, or reliance on incorrect professional advice.

When you don't file, the IRS may eventually file a Substitute for Return on your behalf. An SFR uses the income information reported to the IRS (from your clients' 1099s, your banks' 1099-INTs, etc.) and calculates your tax with:

- No business deductions: The IRS won't claim your home office, vehicle expenses, supplies, or other Schedule C deductions

- No favorable filing status: SFRs typically use "single" or "married filing separately"

- No credits: No earned income credit, child tax credits, or education credits

- No adjustments: No deductible half of self-employment tax, no IRA deductions, no HSA deductions

The result: an SFR almost always shows a much higher tax liability than what you'd owe if you filed yourself. If the IRS has filed an SFR for any of your missing years, you can (and should) file your own return to replace it. Your actual return will supersede the SFR.

Here's a detail that costs people thousands of dollars: if the IRS owes YOU money, you only have 3 years from the original due date to claim it (IRC §6511).

For example:

- 2022 return (due April 15, 2023): Refund claim deadline is April 15, 2026

- 2023 return (due April 15, 2024): Refund claim deadline is April 15, 2027

If you had expenses that exceeded your income in a given year, or you're entitled to refundable credits, filing late can still put money in your pocket, but only if you're within the 3-year window. After that, the refund is forfeited permanently.

For self-employed individuals: Even if you owe tax for most years, check each year individually. You might have had a slow year where deductions exceeded income, making you eligible for a refund. File those years first to capture the refund before the deadline expires.

Filing back taxes isn't just about settling old debts. Being "in compliance" with the IRS affects several other areas:

- Passport renewal/application: The IRS can certify your tax debt to the State Department if you owe more than $66,000 (the seriously delinquent tax debt threshold for 2026 under IRC §7345, adjusted yearly for inflation), which can result in passport denial or revocation

- Mortgage applications: Lenders typically require two years of filed tax returns

- Business loans and SBA loans: Require filed returns for all open years

- Installment agreements and OICs: You must file all required returns before the IRS will consider a payment plan

- Social Security credits: If you don't file self-employment returns, you don't receive credit for those earnings toward Social Security retirement benefits

- Statute of limitations on audits: The IRS's 3-year audit window doesn't start until you file. If you never file, the IRS can audit that year forever

The failure-to-file penalty is 10x the failure-to-pay penalty. File the return even if you can pay nothing. It stops the 5% monthly penalty and starts the clock on the statute of limitations.

When you're anxious about back taxes, it's tempting to rush through the returns. But skipping legitimate deductions means overpaying. Take the time to reconstruct your business expenses from bank statements. Every deduction reduces both income tax and self-employment tax.

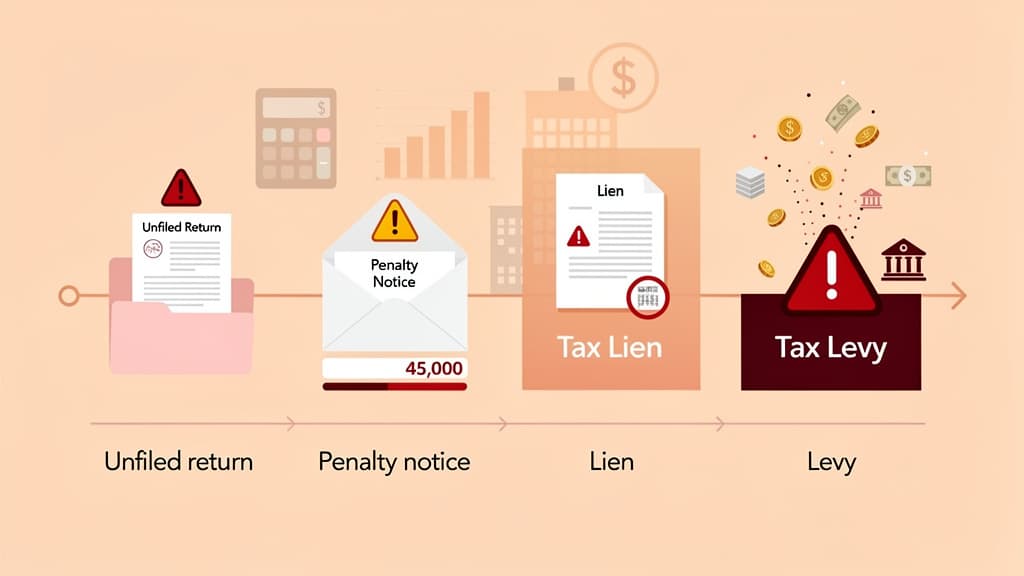

IRS notices escalate in severity. The progression typically goes: CP14 (balance due) → CP501 (reminder) → CP503 (urgent) → CP504 (intent to levy) → LT11/Letter 1058 (final notice of levy). Responding early gives you more options.

Some companies charge thousands of dollars upfront to "negotiate" with the IRS. Before paying anyone, file your returns yourself (or with a CPA/EA). Many people discover their actual liability is manageable once deductions are applied. You don't need a negotiator if you can set up a $200/month installment agreement online for free.

If the IRS owes you a refund for any year, the clock is ticking. Prioritize filing any year where you might be owed money and the 3-year window is about to close.

The best way to deal with back taxes is to never fall behind again. For freelancers and self-employed business owners, that means tracking income and expenses throughout the year, not scrambling at tax time.

Jupid connects directly to your bank accounts and categorizes every transaction automatically with 95.9% accuracy. Instead of sorting through a year's worth of statements to reconstruct your Schedule C, your books are maintained in real time.

Jupid's AI accountant is available on WhatsApp and iMessage, so you can check your profit, estimated tax liability, or deduction totals anytime, with no logging into software and no appointment with an accountant. Ask "How much do I owe in estimated taxes this quarter?" and get an answer in seconds.

For people who have fallen behind, getting organized going forward is half the battle. Once your current-year taxes are under control, filing on time becomes the default rather than the exception.

Get organized with Jupid →

- IRC §6511: Limitations on credit or refund (3-year rule for refund claims)

- IRC §6651(a)(1): Failure-to-file penalty (5% per month, max 25%)

- IRC §6651(a)(2): Failure-to-pay penalty (0.5% per month, max 25%)

- IRC §6601: Interest on underpayment of tax

- IRC §7122: Offers in Compromise authority

- IRC §6159: Installment agreements

- IRC §7345: Seriously delinquent tax debt / passport certification ($66,000 threshold for 2026)

- IRS Policy Statement 5-133: Delinquent returns, enforcement of filing generally limited to the past six years

| Item | 2026 Amount |

|---|

| Standard deduction (single) | $16,100 |

| Standard deduction (MFJ) | $32,200 |

| SE tax rate | 15.3% |

| Social Security wage base | $184,500 |

| Minimum late filing penalty | $525 (returns over 60 days late, filed in 2026) |

| Failure-to-file penalty | 5%/month, max 25% |

| Failure-to-pay penalty | 0.5%/month, max 25% |

| Interest rate (Q3 2026) | 7% (short-term rate + 3%), compounded daily |

| Years to file for compliance | Generally last 6 (Policy Statement 5-133) |

| Streamlined installment agreement limit | $50,000 |

| Passport certification threshold | ~$66,000 |

Filing back taxes feels overwhelming, but the process is straightforward once you start: gather documents, use the correct year's forms, claim every deduction, and file. The IRS offers multiple payment options for balances you can't pay in full.

The most expensive decision is doing nothing. Every month of inaction adds penalties and interest, and keeps you locked out of loans, payment plans, and the peace of mind that comes with being in compliance.

Disclaimer

This article provides general information about filing back taxes and should not be considered tax or legal advice. Penalty calculations, interest rates, and IRS program eligibility depend on your specific circumstances. The IRS Fresh Start Initiative criteria and payment plan terms are subject to change. For advice specific to your situation, consult with a qualified tax professional, enrolled agent, or tax attorney.

Tax Year: 2026

Last Updated: July 7, 2026